Most drivers in Dubai spend more time choosing their car color than choosing their insurance policy. That is understandable. Insurance is not exactly exciting. But the people who rush through it tend to be the ones standing at a repair shop months later, learning for the first time what their policy actually covers. A little time spent up front saves a lot of frustration later.

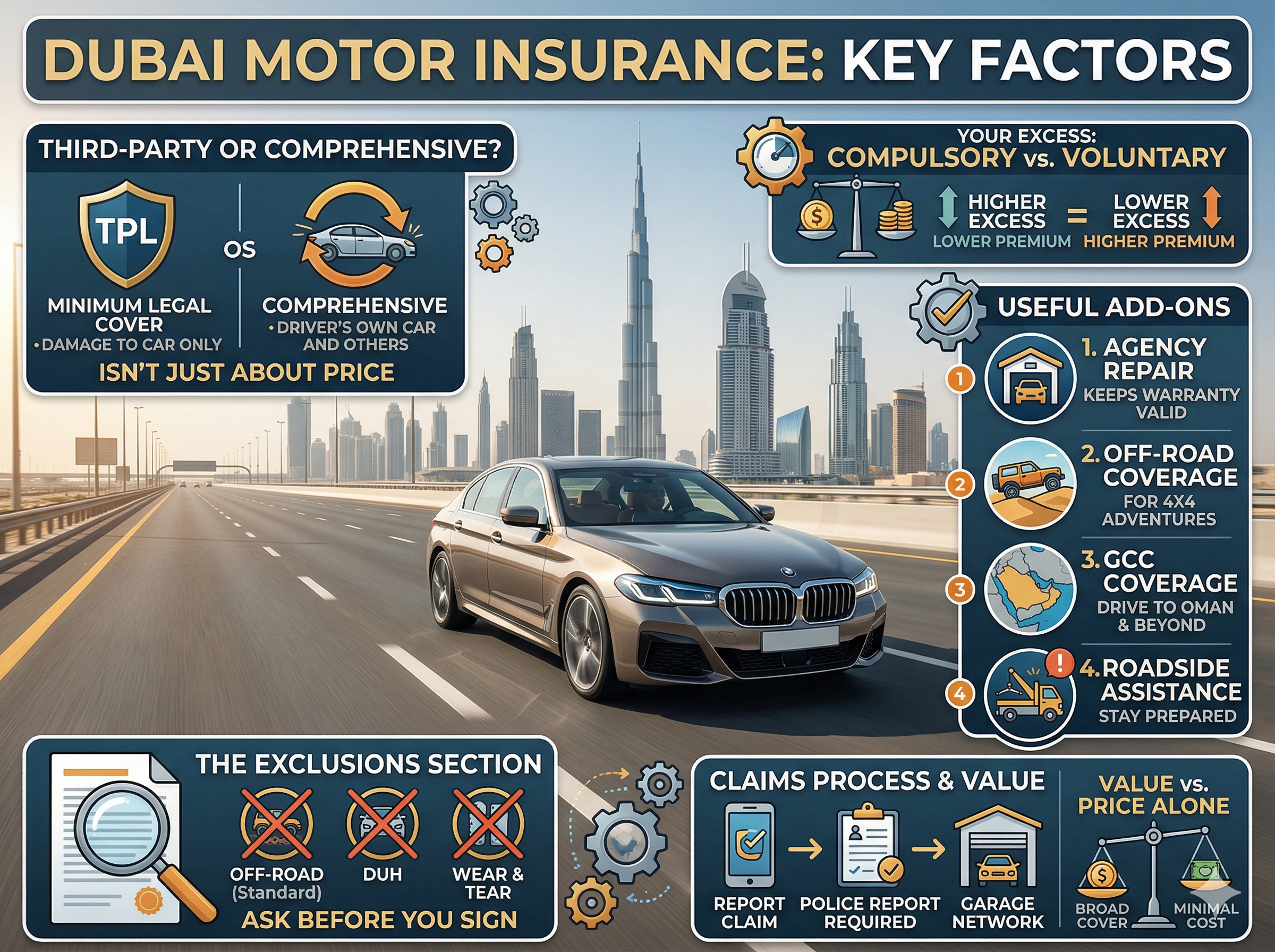

Third-Party or Comprehensive: Why It Is Not Just About Price

Third-party liability (TPL) is the legal minimum in the UAE. It pays for damage you cause to other people’s vehicles or property, but if your own car gets damaged, whether in a collision or after something like flash flooding, the repair bill is yours. Comprehensive coverage includes your vehicle as well.

For a newer car, going comprehensive is almost always the right call. The cost of a single repair on a recent model can wipe out several years of premium savings from choosing TPL. For an older vehicle with a low market value, the equation changes. Paying comprehensive premiums on a car worth AED 15,000 may not make much financial sense. It is better to base that decision on your actual car and its value, rather than following a blanket rule.

The Exclusions Section Is Where Surprises Hide

Nobody reads the exclusions until they have to. That is exactly the problem. The moment you file a claim is the worst time to discover that the damage you are claiming for falls into a category your policy never covered.

Common exclusions across UAE policies include:

- Off-road damage, unless you have added a specific off-road extension

- Accidents that occur while driving under the influence

- Mechanical or electrical failure not caused by a collision

- Gradual wear and tear

- Flood damage in certain areas, depending on how the policy defines the event

Ask your insurer to walk you through the exclusions before you sign. If they cannot explain them clearly, or if the answers feel vague, that tells you something about how the relationship will go when you actually need to make a claim.

Choosing Your Excess: The Trade-Off Most People Get Wrong

The excess is the amount you pay yourself before the insurer covers the rest. A higher excess usually brings the annual premium down, which can look like an easy saving at first, until you need to make a claim and suddenly have to come up with that amount on the spot.

UAE policies usually come with a compulsory excess set by the insurer, and in some cases a voluntary excess you can add to reduce the premium further. Choosing a higher voluntary excess can make sense, but only if paying AED 2,000 or AED 3,000 yourself in an emergency would not put you under pressure. Saving AED 300 a year is not really a win if it leaves you short when you need the cover most.

Add-Ons That Are Actually Useful Here

Add-ons vary wildly in how useful they are, depending on the driver. A few stand out as particularly relevant to the UAE context:

1. Agency repair: Your car goes to the manufacturer’s authorized workshop, not a general garage. For vehicles still under manufacturer warranty, using a non-agency workshop can void that warranty, so this add-on pays for itself if your car is relatively new.

2. Off-road coverage: Standard policies explicitly exclude off-road terrain. If you own a 4×4 and actually take it off-road (even occasionally), you need this extension. Without it, damage from anything other than paved roads will not be covered.

3. GCC coverage: Driving to Oman or Saudi Arabia without checking your policy’s territorial limits is a common oversight. A GCC extension ensures you are covered across borders, not just within the UAE.

4. Roadside assistance: Breakdowns in 45-degree heat are not a minor inconvenience. Towing, battery recovery, tyre changes: having this covered removes a genuinely stressful situation from the equation.

Go through add-ons based on how you actually use your car, not how you imagine you might. A GCC extension is pointless if you never drive across the border. Agency repair matters a great deal if your car is two years old and considerably less if it is ten.

Claims: What the Process Looks Like on the Ground

The claims process is where most people form their real opinion of their insurer, usually under stress, after an accident. Before you commit to a policy, find out: Can you report a claim through an app, or does everything go through a phone line? How quickly does initial acknowledgment come? Which garages are in their network, and do those garages have a decent reputation?

In the UAE, a police report is required before any insurer will process a claim. This applies even to minor accidents. If you have never been through this before, knowing the procedure in advance (report online via the relevant emirate’s traffic app, get the reference number, then contact your insurer) prevents the kind of delays that happen when people try to figure it out in real time.

Online reviews for insurers in this market are mixed and sometimes unreliable, but patterns across multiple reviews tend to be telling. If the same complaint shows up repeatedly across different platforms, slow response, disputed claims, and unresponsive support, take it seriously.

Why Comparing on Price Alone Rarely Ends Well

When comparing motor insurance Dubai quotes, two policies at the same price can cover very different things. One might include agency repair and a broad GCC extension; the other might restrict repairs to a handful of garages and exclude weather-related damage. The premium looks identical. The actual coverage does not.

Compare the coverage scope line by line, not just the bottom-line cost. A policy that costs AED 400 more per year but includes agency repair and a responsive claims process is almost always a better value than the cheaper alternative, especially for anyone driving a car worth more than AED 60,000.

Also, check that the insurer is licensed by the UAE Insurance Authority. This matters practically: if a dispute arises, the Insurance Authority gives you a formal complaints channel. With an unregistered provider, you have considerably less recourse.

Your Car’s Age and Condition Affect More Than Just the Premium

Insurers price risk based on the vehicle’s make, model, age, and current market value. Older cars attract lower premiums under comprehensive policies, but they may also face stricter conditions. Some insurers apply higher excess amounts to vehicles above a certain age, or reduce the payout based on depreciation in ways that catch drivers off guard.

Modifications are another area where people get caught out. Aftermarket upgrades (audio systems, body kits, performance modifications) generally fall outside standard policy coverage unless you have declared them. If your car has been modified and you do not mention it, you risk having a claim partially or fully rejected. Disclose it when applying; most insurers will either cover it or tell you upfront that they will not.

Getting It Right Before You Need It

Insurance decisions tend to feel low-priority right up until the moment they become the only thing that matters. The drivers who end up satisfied with their coverage are usually the ones who treated the selection process as seriously as any other significant purchase, not in a complicated way, but in a deliberate one.

Read the exclusions. Match the add-ons to your actual driving habits. Set an excess you can genuinely afford. Ask how claims work before you ever have to make one. None of this takes long, and all of it pays off when the situation is no longer hypothetical.